Insights for

Financial Success

Turning Your Job to an Asset – A Business Transition Plan

There can be a lot of different motivations for starting a business, but typically, business owners pursue this path for one of the following reasons:

- Income

- Flexibility

- Asset growth

While many founders are successful at the first two, asset growth is often a struggle. This is why viewing a business as an asset rather than a job can be a transformational shift in perspective.

Whereas a job is something you have to work at—you show up, and if you don’t, you don’t get paid—an asset is something that typically grows and pays you, and doesn’t necessarily require you to work.

Understanding this difference can have a big impact on the outcome of your business in the long term.

Why does this matter?

According to the Exit Planning Institute, although 76% of business owners plan to transition in the next 10 years, almost half of them (49%) don’t have any exit plan at all.

The result? 70% of businesses listed for sale never actually sell.

For family-owned businesses, the numbers are even more striking:

- Only 30% transition to the second generation.

- Just 12% make it to the third generation.

Even if you’re not thinking about exiting right now, your business transition is an important topic that deserves a lot of thought and consideration—especially when selling might not feel like an urgent matter for you. This gives you more time to plan out an optimal exit strategy so that you’re ready when the time comes, rather than rushing the process when selling becomes more pressing.

Why is transitioning so difficult?

It’s common for business owners to view their business as their baby, and to have a hard time imagining what it would look like without them in the picture. As a result, too many businesses are overly reliant on the owner to generate revenue, which can make the company seem unattractive to prospective buyers.

Another issue that founders face is that the valuation of their company is not high enough for them to live off once they’ve sold the business. As a result, they end up no longer being able to rely on it as a source of income.

Finally—and this is arguably the most important consideration—most owners don’t have a clear vision for what the next chapter of their lives will look like.

The good news is that with the right approach, a business can become a real asset—one that works even when the owner is not directly involved.

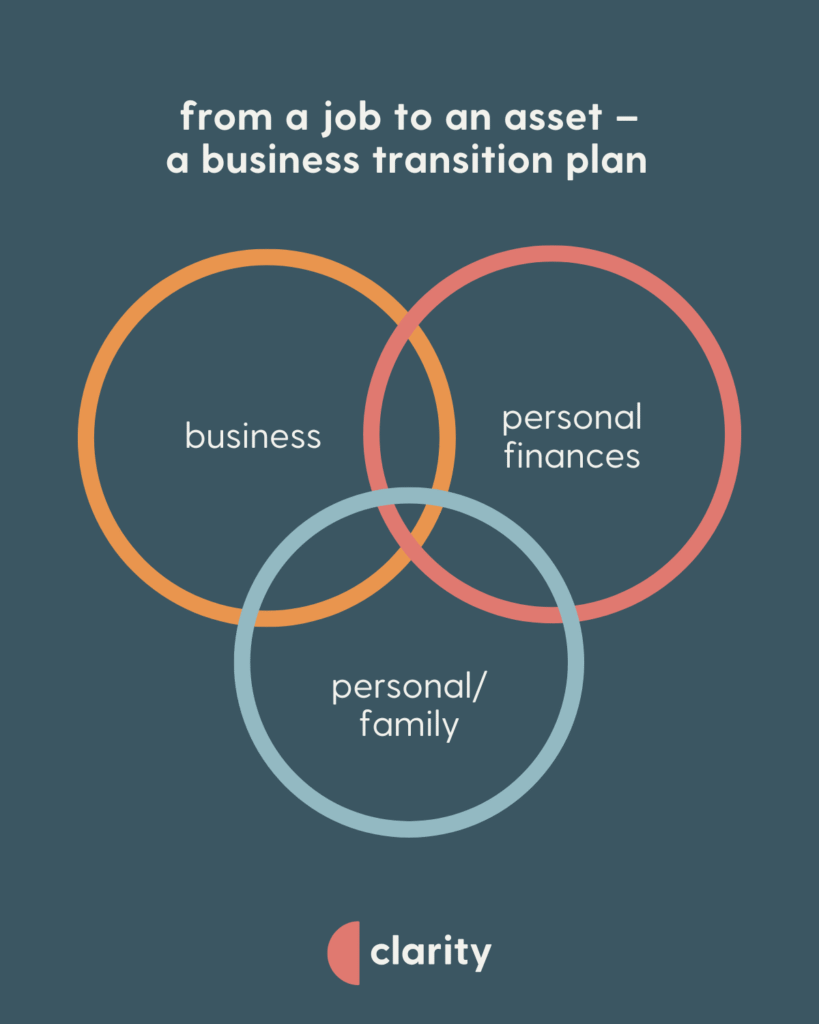

How to transition successfully in 3 steps

In considering a business transition, it can be helpful to differentiate between three areas that it might impact:

- Business

- Personal finance

- Personal/family goals

With that in mind, here are 3 steps to make it easier to transition your business from a job into an asset.

1. Stop treating the business like a job [Business]

This strategy will help you solve the “business” problem. Here’s what you need to do:

- Identify the stage of business you’re at.

Businesses go through different stages as they grow, from survival, where sales and marketing are crucial, to stable, in which you have established a regular client base, but you may be faced with operational or logistical stress as you try to scale to meet the demand for your services/products.

Eventually, once you’ve hired some staff and established repeatable processes, you enter the sustainable stage, where the onus is on the leadership team to figure out what the next chapter of the business will look like.

Knowing which stage of business you’re in will help you determine the next steps that make sense for you.

- Shift your role over time from doer to manager to leader to coach

As mentioned earlier, many business owners fall into the trap of making the business dependent on them to function properly.

This is fine in the beginning, where the founder is usually a “doer,” but you will want to work on moving away from this role in the long term. As you grow your team, you should shift to become more of a manager, delegating tasks you previously took on to appropriate staff members.

As your business becomes more established, you will likely hire managers to run your growing team. This will give you more space to become the leader and focus solely on thinking about the next steps for your business. Finally, you want to get to a stage where the business can operate without you, at which point you become more of a coach to the executives who work for you.

- Put benchmarks and accountability systems in place for revenue, profit, and cash flow

This will allow you to build systems and processes (such as documentation and SOPs) to scale your company and avoid relying on individuals. This is important because if someone leaves the company, you need to make sure that someone else can do their job according to the procedures that you have established.

2. Build an asset mix [Personal finance]

Your first step here is to decide on your ideal exit outcome.

- Do you plan on simply closing the business once you choose to stop working?

- Do you want to sell the business internally (to an employee or family member)?

- Do you want to sell the business externally (to an investor or third party)?

Once you’ve figured that out, you can start to grow your business investment portfolio in a way that matches your intended exit strategy.

There are a variety of investment options to pick from here, including:

- Cash

- Fixed income

- Mutual/segregated funds

- Stocks

- Private equity

- Real estate

All these investment types have different characteristics and pros and cons. Deciding which one is right for you is largely about achieving the right mix to support your desired exit strategy.

In addition to supplementing your business income through the investments listed above, think about what other types of income you may have access to later on in life, including government benefits, group pension plans, personal investments, rental income or maybe even a part-time job.

One option you might not have considered: many of our clients who have sold their business end up becoming part-time consultants or speakers, sharing the knowledge they’ve built over the years of running their own company.

3. Define a financial finish line [Personal/family goals]

What will your life look like after your business?

Think about the important people in your life, what you would like to spend more time doing, what you want your legacy to be, and what your main concerns are with these three considerations.

This will give you the motivation and clarity to build your business in a way that supports your priorities.

That’s why it’s important to start mulling these things over well before it’s time to exit, because some of these questions aren’t easy to answer—and you definitely don’t want to rush them.

How clarity planning can help

We can help walk you through these questions and determine what feels right for you. Some of these considerations require lots of coordination between different areas of your life, which can feel overwhelming. That’s where we come in, to:

- Connect the dots between your business and personal finances

- Prioritize the right steps for a smooth transition

- Help you make confident financial decisions without unnecessary complexity

Contact us today for a free consultation to discuss how you can start transforming your business from a job to an asset.