Blog

How Much Money is Enough? How to Evaluate Your Spending and Saving as a Business Owner

When it comes to money (especially the amount of disposable income we want to have each month), is there an amount that is “enough”? Or is more always better?

As a business owner, it’s common to set ambitious revenue targets and constantly work towards growth—maybe that looks like aiming for $200,000 in sales this year, or a million-dollar business. And maybe, in your financial planning, you’re looking for that “magic number” to work towards to know that you’ve “made it.” But life, business, and finances are messy and don’t often respect those neat categories. After all, what happens if something changes? And what happens when you hit those goals?

The Myth of “More is Better” and the “Magic Number”

As a former business coach, I worked with many successful entrepreneurs. I watched them set and achieve big goals, only to celebrate, rinse, and repeat. I can’t recall one single client that said, “I think I’m good now and don’t need to make any more,” regardless of hitting $1M or $5M or even $10M in sales each year. As we reached the target, the goalpost would move because the client did not feel that they had “arrived.”

Instead, they typically felt like they still needed to make more money. And the fact is, that as revenues increase, expenses often also increase. There is always something that needs to be funded: the budget to hire another staff member, increase inventory, lease a bigger office to house everything, or upgrade systems and infrastructure to support the growth.

Sometimes, wanting to make more money is not just about growing the business, but about wanting to spend extra personal income on things like a new car, a longer vacation, renovations or moving to a new home. And it doesn’t even have to be that extravagant – just a nicer restaurant to enjoy on weekends, eating out slightly more frequently, and buying nicer stuff here and there as you’re able to afford it.

But what is really interesting is that clients often don’t feel significantly happier just because they have a bigger business or they can pay themselves more. So many clients have mentioned to me that they thought they would be happier if they achieved a certain financial goal or reached a business milestone, but in reality, most don’t feel too different when their businesses become more established.

The answer to “How much money is enough?” is not a magic number that will make us happy. If it was, celebrities and the rich would be the happiest people in the world – which we know is not the case. Our culture would have us believe that the more we have, the happier we’ll be. But that’s a myth.

Contentment Is A Choice

So, does this mean that you shouldn’t choose to grow your business once it hits a certain level? Or you shouldn’t aim to make more money once you can cover your expenses?

Absolutely not. Choosing contentment doesn’t mean “playing small” or giving up on growth. It just means growing with purpose.

So, how do you make that happen?

Allocating Your Money Wisely

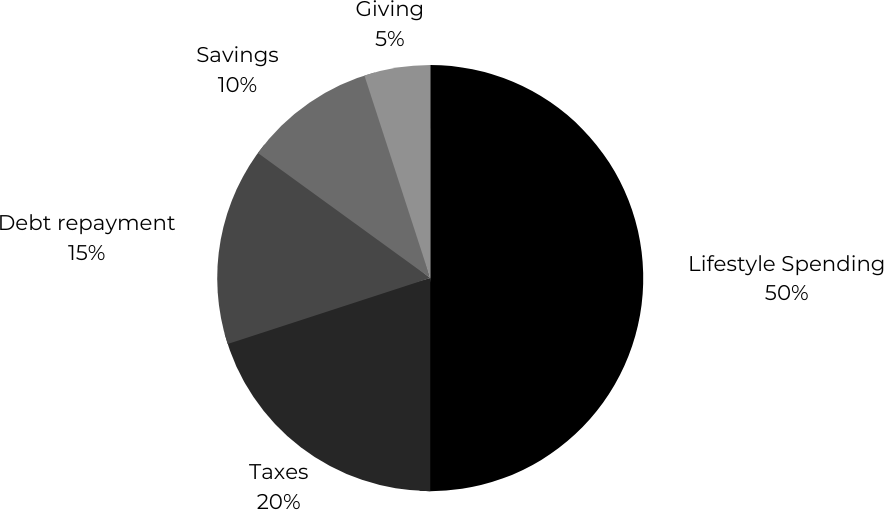

One way to find contentment is to be intentional with your money. Ron Blue, founder of Kingdom Advisors, outlines five categories of spending:

- Lifestyle – paying for food, household expenses, and entertainment

- Taxes – paying income tax installments or property taxes

- Debt – paying mortgage or rent, car loans, or student loans

- Savings – setting aside money in your bank account or investing

- Giving – donating to charity

A pie chart is a helpful way to look at this because the decisions you make in one segment (whether consciously or unconsciously) impact the amount of money leftover in other segments. For example, if you have more debt, you might have less to spend on saving or giving.

But regardless of how much income you have, everyone has the same decisions to make: how much money do I want to allocate to each segment?

Many clients find it eye-opening to do this exercise, because they often don’t realize how much they are spending in each category. When asked, most would prefer to allocate more to savings or to be able to give at least a bit more, but they just don’t feel that there is anything leftover to give at the end of each month.

I don’t know too many people that “accidentally” have a lot of leftover funds for the “Grow” and “Give” category. Usually there are more people that accidentally spend more on lifestyle, debt, or paying taxes.

A potential solution is simply to change the order in which we allocate our funds when it hits our bank accounts. By shifting your spending order—for example, by starting with debt, then paying taxes, followed by, giving, and finally lifestyle—you can better align your spending with your values. In other words, by consciously deciding how to allocate your money, you can ensure that you’re funding what’s important to you, both in business and in life.

Here’s what to ask yourself:

- Are you satisfied with how your funds are currently allocated?

- What are the short term and long-term consequences of the current allocations?

- If you are not satisfied with the allocation, what do you want it to be instead?

- What would be the short term and long-term consequences of the desired allocations?

I would encourage you to check what your allocations are currently in order to become more aware of your current situation, and then determine if you want to change the allocations for the future. Head to financiallysmartbusiness.com to download a spreadsheet to track for the next few months.

Moving (Slowly) In The Right Direction

Changing your financial habits takes time. If you feel that your current allocations are far from ideal, start small: adjust the categories by 1% each month until you gradually align your spending with your values.

Within your business, this exercise may be slightly easier because you likely already have some financial systems in place to track monthly revenues and expenses. I would encourage you to review your expenses periodically with your bookkeeper and accountant, to check whether spending in each category (for example: labour/salaries, materials, marketing, training, rent/leases, insurance, utilities, interest, professional fees, etc.) are in line with best practices for your stage of business in your specific industry.

When you review your business financials, it’s good practice to track and report each category as a percentage of your revenues, so that over time, you can determine if the percentage of expenses is in line with your revenue growth over time. This can easily be done through most accounting software. As your company grows, you can then determine if the percentage of spending for each category is in line with the revenue growth, and adjust your budget accordingly to ensure that you remain profitable as revenues grow.

Finding A Balance

Of course, you can consult with a financial planner to optimize your allocations and ensure that your financial strategy supports both your business growth and your personal happiness. Book a call and we’d be happy to help you with this!

In business, just like in life, the pursuit of “more” won’t necessarily make you happier or more successful. By making intentional choices around how you allocate your money and—more importantly, why you’re working towards making more in the first place— you can find a great balance between growth and happiness.